[ad_1]

solarseven/iStock via Getty Images

Investment Thesis

During the recent Investor Briefing on 7 April 2022, CrowdStrike (NASDAQ:NASDAQ:CRWD) demonstrated its market-leading edge in providing its cybersecurity Falcon platform through cloud-native, AI-driven technology. Despite its rather early introduction in 2011, the company’s offering proved to be highly relevant in recent years, primarily through the remote work and boom of cloud servers during the COVID-19 pandemic. In addition, US critical infrastructure has been the target of widespread cyberattacks by the Russian government since 2014, which have been exacerbated by the ongoing war in Ukraine. These factors have made cybersecurity more important than ever.

In the briefing, CRWD demonstrated why the company had been the leader in Endpoint Detection and Response market for the past two years, and why it will continue to be so.

Cyber Security Has Never Been More Relevant

Migration To Cloud Servers In 2020 During COVID-19

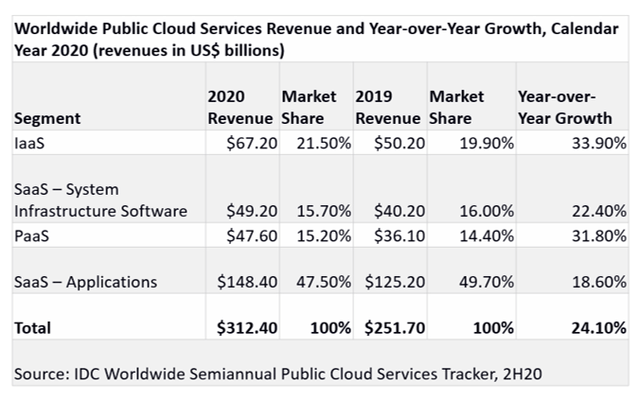

Reproduced from International Data Corporation

Based on McKinsey, during the height of the COVID-19 pandemic, a mass enterprise migration from conventional servers to digital servers punctuated the importance of cloud-native, AI-driven cyber security technology. Based on International Data Corporation, adoption for Public Cloud Services grew 24.1% YoY from $251B in 2019 to $312B in 2020, with the SaaS System Infrastructure Software reporting 22.4% YoY growth and SaaS Applications 18.6% YoY growth.

The growth in Public Cloud Services was also projected to accelerate by 26.1% YoY to $396B in 2021. CRWD reported over 5K customers deploying Falcon in the public cloud setting, representing an impressive 20% growth QoQ with $106M ARR in FY2022. Furthermore, the global cloud computing market is expected to further grow to $947.3B in 2026, at a CAGR of 16.3%. Therefore, we anticipate the adoption of cloud services and their related cyber security services to grow rapidly in the next few years.

CRWD As A Leader In The EDR Market

CrowdStrike

During its recent Investor Briefing on 7 April 2022, CRWD further elaborated on its mission to provide its customers with the cyber protection that demonstrated its leading vision since 2011. Its relevance in the Endpoint Security Market is also evident through its increased market share, from 7.9% in CY2019 to 14.2% in mid-CY2021. Furthermore, we expect CRWD’s market share to increase over time, given that the global cybersecurity market is expected to grow from $133.5B in 2021 to $211.7B in 2026, at a CAGR of 9.68%.

In addition, consensus estimates that the US market will account for most revenue generated at 40% in 2022. Given that US President Biden had also stressed the importance of cybersecurity in the wake of the ongoing crisis in Ukraine, we expect CRWD’s Falcon Platform to be adopted by more US government agencies and major enterprises moving forward.

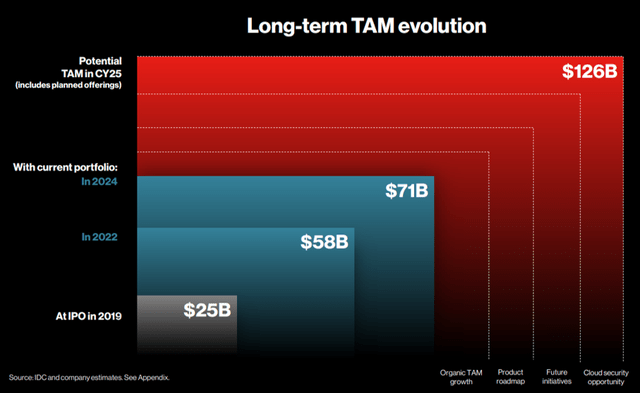

CRWD Total Addressable Market

CrowdStrike

CRWD also iterated its confidence in achieving $5B Annual Recurring Revenue (ARR) by FY2026, expanding its Total Addressable Market to $126B by CY2025 through its existing modules, future initiatives beyond endpoint security, and cloud security opportunities. As a result of Falcon’s flexibility in use cases and unified back end, the company will be able to provide massive scalability across various deployments, value, and operational efficiency in the long run.

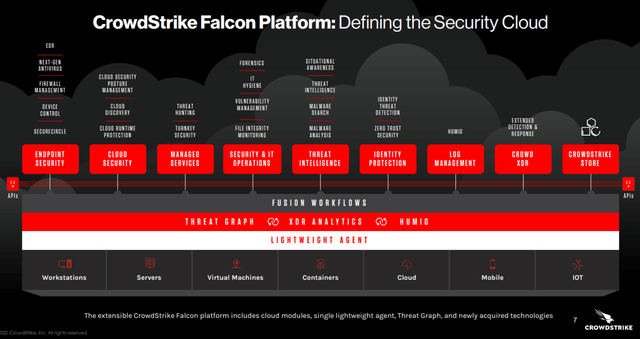

CRWD Scalable Product for Multiple End Markets

CrowdStrike

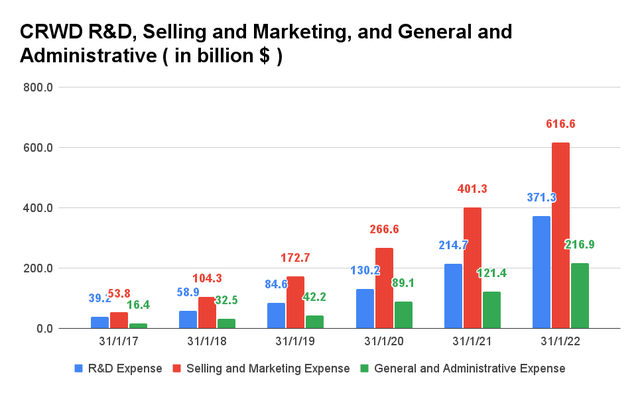

Since its IPO in 2019, the company has also expanded its platform from ten modules to 22 modules as of April 2022. As a result, it is evident that CRWD has been actively investing in its pipeline through increased R&D expenses, at a CAGR of 56.78% since CY2017. In FY2022 alone, the company spent $987.83M for R&D and Selling and Marketing Expenses, representing a whopping 68% of its revenue then, with a staggering increase of 60.3% YoY. Given the company’s ambition in penetrating different markets beyond the traditional endpoint security, we expect CRWD to continue its aggressive R&D and Selling and Marketing Expenses in the next four years.

CRWD R&D, Selling and Marketing, and General and Administrative Expenses

S&P Capital IQ

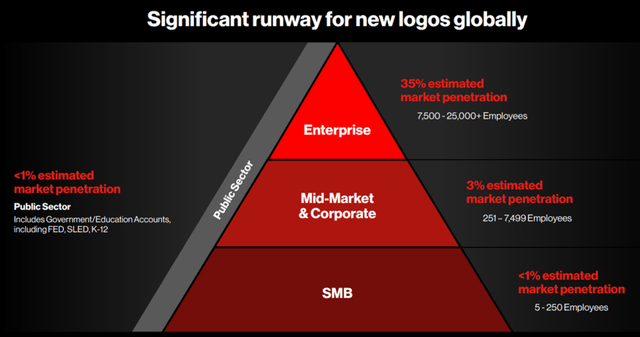

CRWD’s Future Opportunities

CrowdStrike

In addition, given CRWD’s scalable modules, the company has been able to penetrate multiple end markets of different sizes, most notably the Enterprise segment at 35%. To date, CRWD estimates significant opportunities in three other segments where its penetration has been lagging, namely:

- Mid-market & corporate – 3% market penetration.

- Small and Medium Businesses (SMB) – less than 1% market penetration.

- Public Sector – less than 1% market penetration.

Given that the SMB and the mid-market comprised 99.9% of all US businesses at 32.5M in 2021, CRWD’s market opportunity is massive, once more and more realized the need to transition to the cloud server. Globally, the company is also extending its reach into the EU with its partnership with Orange Cyberdefense in offering the Falcon platform to SMBs there.

Its opportunities in the public sector are just starting as well, since CRWD was recently granted a Provisional Authorization to Operate (P-ATO) at Impact Level 4 (IL-4) from the US Department of Defense (DoD) on 7 April 2022. The new authorization will allow the company to deploy its Falcon® cybersecurity platform for a broad range of critical assets protections under DoD and Defense Industrial Base (DIB). Furthermore, with a forthcoming Level 5 authorization, it is evident that CRWD is delivering on its promise to help secure National Security Systems, similar to Palantir (PLTR) with Impact Level 6 DoD Authorization. In FY2021, PLTR recorded $897M in revenues from 90 government customers with a CAGR of 52.08% in the past three years, with $678M attributed to the US government with a CAGR of 58.58%.

In addition, the German government also added CRWD to the Federal Office for Information Security (BSI) list of qualified Advanced Persistent Threat (APT) response service providers on 13 April 2022. Similar to the authorizations received from the US DoD, the list acknowledges the company’s qualification in providing the expertise needed to mitigate and handle any potential cyberattacks for any German companies, critical infrastructure operators, and government institutions. Though CRWD does not break down its revenue based on customers, we expect the company to record incremental opportunities and revenue growth while serving the public sector globally.

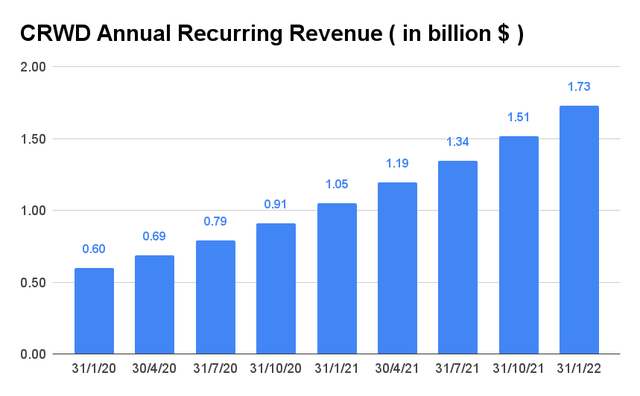

CRWD Report Excellent Growth In FY2021

CRWD Annual Recurring Revenue

S&P Capital IQ

CRWD reported 64.7% YoY growth in its ARR, from $1.05B in FY2021 to $1.73B in FY2022. It reflects tremendous demand for its business, given the 68.9% YoY growth in the company’s subscription from $805M in FY2021 to $1.36B in FY2022. In addition, the company added a record-breaking ARR of $217M in FQ4’22, representing an increase of 27.6% QoQ with accelerating growth in the second consecutive quarter. The growth was mainly attributed to robust demand in enterprise contracts and public cloud segments.

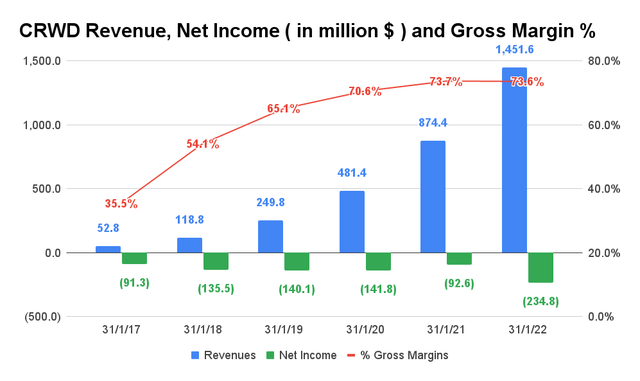

CRWD Revenue, Net Income, and Gross Margin

S&P Capital IQ

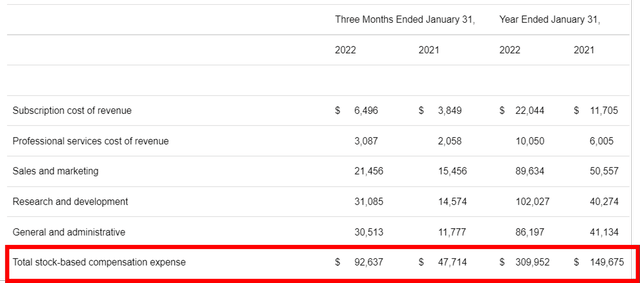

In the past five years, CRWD reported massive growth in its revenue at a CAGR of 94.02%. In FY2022 alone, the company reported revenues of $1.45B, representing an increase of 66% YoY, with robust gross margins of 73.6%. However, it is clear that CRWD has yet to report net income profitability at -$234.8M in FY2022. Part of this is attributed to its massive stock-based compensation expenses, which more than doubled YoY, from $149.6M in FY2021 to $309.9M in FY2022. Nonetheless, investors must also note that since its IPO in June 2019, the company’s shares have been diluted by 12.5%, from 204.1M shares in FQ3’20 to 229.7M in FQ4’22.

CRWD Stock-Based Compensation

Seeking Alpha

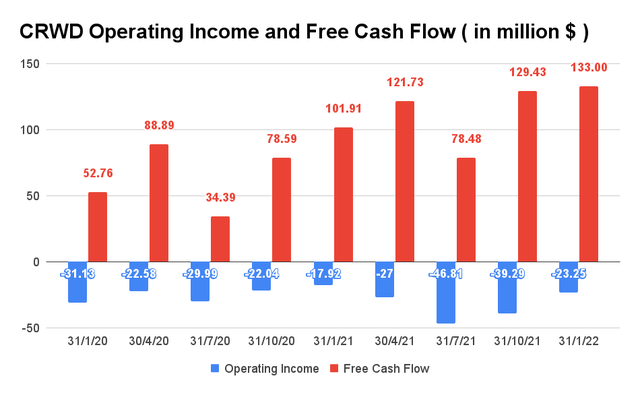

CRWD Operating Income and Free Cash Flow

S&P Capital IQ

CRWD reported robust Free Cash Flow (FCF) of $512M for the last fiscal year, excluding the effects of IP transfer tax payment for its acquisition of Humio. It is also important to note that the company has been reporting positive FCF since FQ3’20. As a result, we are not concerned about its lack of net income profitability yet, given its excellent execution.

So, Is CRWD Stock A Buy, Sell, or Hold?

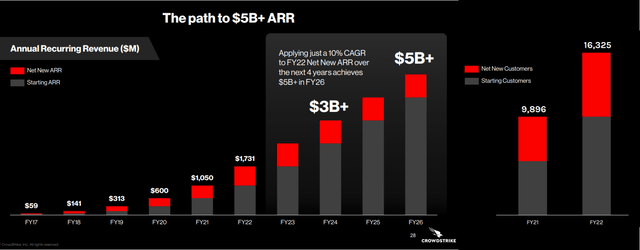

CRWD Projected Annual Recurring Revenue & Growth In Customer Base

CrowdStrike

On its Investor Briefing, CRWD raised its ARR guidance higher from the previous year, from a CAGR of 14.74% to 30.37% for the next four years, with a cumulative ARR of over $5B by FY2026, instead of the previous $3B. The impressive numbers further highlighted its accelerating growth, expanding customer base, and high retention rates, despite the reopening cadence post-COVID-19. It is evident that cloud-based services are here to stay and will continue to change the way the world operates in the future. For FY2023, the company also guided revenues in the range of $2.13B to $2.16B, representing an impressive 48.2% YoY growth. In the meantime, consensus estimates that CRWD will finally report net income profitability at $270M in FY2023. In addition, the company guided revenues in the range of $458.9M to $465.4M in FQ1’23, representing excellent increases of 7.9% QoQ and 53.6% YoY.

CRWD is currently trading at an EV/NTM Revenue of 24.63x, lower than its historical mean of 28.81x. However, the stock is trading at a premium of $235.22 on 14 April 2022, up 50% since its 52 weeks low of $156.77 on 8 March 2022. Given the recent rally, CRWD stock is also trading way above its historical 50-day moving average of $190.10 and 200-day moving average of $230.59. Despite CRWD being a solid stock, there is currently no margin of safety, resulting in higher cost averaging for long-term investors. As a result, we encourage investors to wait for a deeper retracement before adding to their portfolio.

Therefore, we rate CRWD stock as Neutral for now.

[ad_2]

Source link