[ad_1]

viper-zero/iStock Editorial via Getty Images

In this article, I’m going to be updating you on my investment in the German Defense company Rheinmetall AG (OTCPK:RNMBY) (OTCPK:RNMBF).

The company is one of the largest defense companies in Germany. It has a history that goes back well over 130 years, a market cap of around €6.6B, and it’s one of the companies that has seen perhaps the most interest from the recent changes in German defense policy.

In this article, we’ll continue answering the question that you might be asking if you’re looking at the current European situation and how the market is developing – namely, should you be investing in Rheinmetall at this time?

Rheinmetall – Revisiting the business

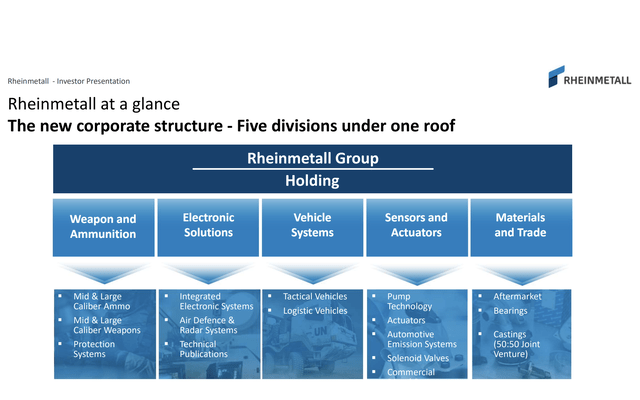

The company is, as I mentioned in my original piece, one of the very few arms manufacturers that remain after two world wars and a cold war. It works in Aerospace, vehicles, weapons, and defense. It’s also one of the few German companies that manufacture ammunition.

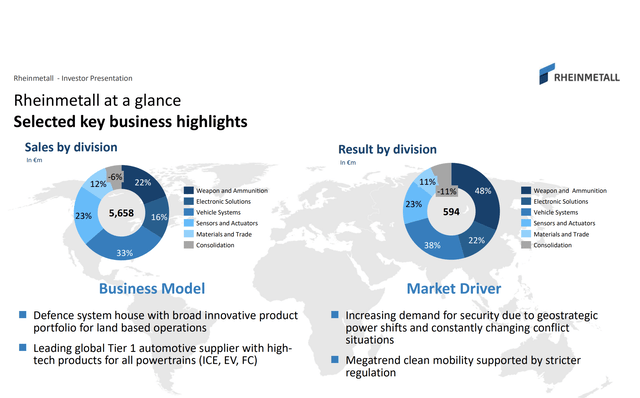

It’s segments are:

- Weapons & Ammunition with large/mid-caliber weapons and their munitions, weapon stations, protection systems, powder, etc.

- Vehicle Systems, focusing on armored Bandwagons, ABC, Tower systems, Logistical Radar vehicles, Tactical vehicles, and a service sub-segment.

- Electronic Solutions, focusing on anti-air systems, guidance systems, sensors, Cyber Security, simulations, etc.

- Sensors & Actuators focus on Solenoids, Materials, Pump Tech, Emission, and Thermo Systems and Actuators.

- Aftermarket, such as Bearings, Casings, and Pistons.

Rheinmetall presentation (Rheinmetall IR)

Rheinmetall is also a somewhat unique play because it diversified away from the pre-Ukraine declining defense industry to head more into the automotive sector, supplying aftermarket parts. While the defense industry/sector revenues are obviously in focus now, it’s essential to realize that this company is as much a play on automotive as it is defense.

The company is a leading, Tier-1 automotive supplier with high-tech products across the ICE, EV, and FC value chain, with components and subsystems for hydrogen technology as well.

This revenue split means that fundamentally speaking, Rheinmetall is in a very good position to really take advantage of the increased geopolitical instability we’re seeing here. With other segments seeing tailwinds due to ESG, EV, and green tech as well as hydrogen, the company is in an excellent spot to really see its revenues increase moving forward.

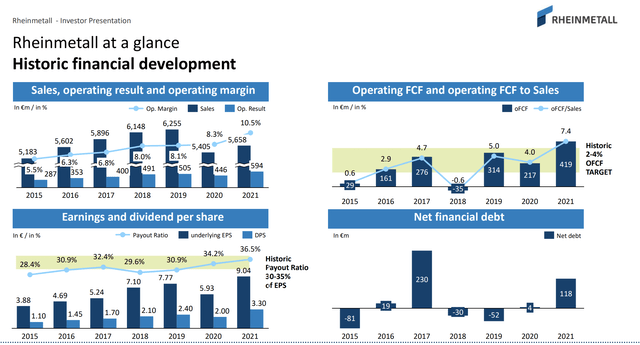

The company is also a surprisingly able and stable dividend payer, with not even COVID-19 making that much of a dent in the dividend record. The company has no credit rating worth mentioning, but also has zero debt. It has a net debt/EBITDA of -0.02X as of 2021E.

Rheinmetall Presentation (Rheinmetall IR)

All of these advantages continue, and since I wrote my last article on Rheinmetall, the following has happened.

When the war started, guidance for defense companies like Rheinmetall went from conservative and negative, to explosive and positive. These initial bumps were extremely rough estimates because no one knew the full impact of the new geopolitical macro, and how serious this situation would turn out to be.

Rheinmetall Presentation (Rheinmetall IR)

These answers are slowly materializing and we can work with an increasing degree of granularity on some of these questions. The situation is clearly more serious than most people expected, which means that some of the more positive assumptions for businesses like Rheinmetall aren’t so outlandish.

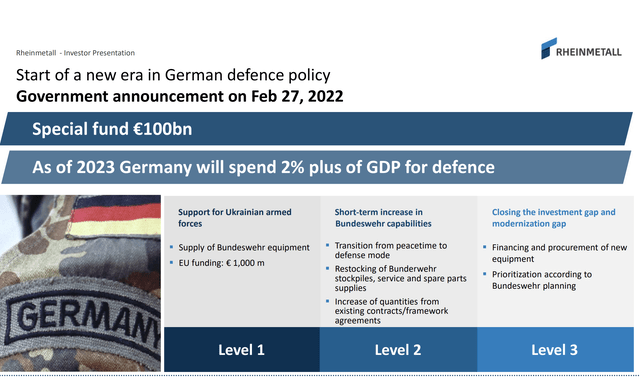

Despite the explosive surge in company share price following Germany’s announcement of a 180 shift in its defense strategy, there is still upside to capture in Rheinmetall. The German government has announced that the €100B would be spent exclusively on the armed forces, whereas there were previous talks about splitting the budget to invest in cybersecurity and partner’s security forces.

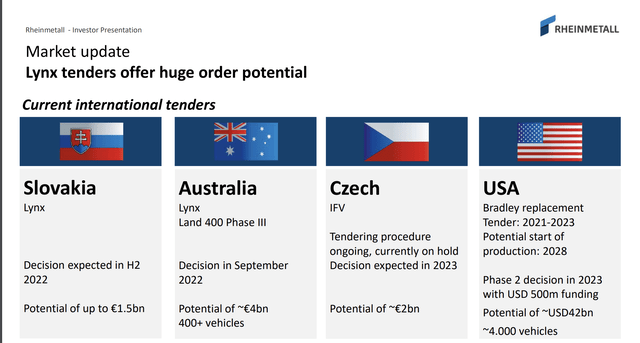

This could have the net effect of broadening Rheinmetall’s potential share of the bill. Initially, Rheinmetall expected up to €42bn of orders and one catalyst might be the officialization of anything close or above. The full impact is still very unclear, but what seems clear is that Germany is very serious about beefing up security across the board. The company has been winning contracts without pause for the past few months, focusing on supplying ammo, air defense systems, light artillery cannon contracts, and new JVs.

The defense industry, which was at a standstill prior to Ukraine, is now firing on all cylinders. Something that younger people that don’t remember the cold war, including myself (born 1985), never thought would happen in Europe again.

Rheinmetall Presentation (Rheinmetall IR)

Based on the projected budget spend, the explosive growth in the company’s share price is not exuberant in the least. It might even, as I see it, be somewhat underestimated. I view the new defense budget projections as completely changing the next 10 years for Rheinmetall.

The company has already identified €42B in sales, and this is likely only the beginning, given that most of the segments have sales periods and contract lengths of between 5-12 years. Expectations for order intakes are up massively. The geopolitical macro means that not only is Germany “tooling up”, but the tailwinds are coming from the entire world.

Rheinmetall Presentation (Rheinmetall IR)

So – tailwinds are significant. I’m moderating my EPS guidance somewhat for the years 2022 and 2023 due to slightly overestimating ammunition spend and underestimated vehicle spend. But the adjustment is slight – less than 5% for 2022E.

On a high level, I still expect a 22.5% EPS growth this year, followed by another 33% in 2023, and yet another 24% in 2022. Military spending is on the rise, and Rheinmetall is absolutely one of the primary beneficiaries of these trends.

Let’s look at valuation.

Rheinmetall Valuation

Rheinmetall’s valuation remains a very interesting exercise to engage in. This is because, in terms of book values, dividend yield, P/E, and other peer-based multiples, the company is currently at quite a bit of premium, ranging from a 10-35% overvaluation.

However, these measurements obviously completely fail to take into account the overall impacts of the increased budget. This is something we find in our DCF and forecast models, which instead point to an undervaluation of over 70%.

This is a very tricky difference to reconcile – but I view the upside as relatively certain. This is because we’re talking about planned government spending. Given the current macro, it’s exceedingly unlikely that there will be back-stepping here. Rather, we’ll see more spending, I believe which will further provide upside to the DCF here. We’re already expecting EBITDA to more than double until 2025 on the basis of 2021A, and based on a current WACC of 9.3%, the implications are for Rheinmetall to be worth no less than €330 per share on a DCF basis.

You may view this DCF estimate as somewhat exuberant – but I reiterate to you, that these are government spending plans, and there are very few alternatives to the capacities that Rheinmetall contextually offers in Germany and to the government.

While it is theoretically possible that the government could back-track if the war ends tomorrow, I believe the current macro marks a fundamental shift in the handling of the east/west dynamics in Europe. I am of the camp that believes that we’re looking at re-erecting the “iron curtain” between the former Soviet Union and overall Europe.

If this is so, then we should align ourselves accordingly with companies that can net advantages from such a development. Rheinmetall is one such business, and it’s fair to say that I believe the company’s advantages will continue, not deteriorate or grow less in any way.

Now, analysts following Rheinmetall are around 11, and 7 of them have either a “BUY” or “outperform” based on a target range of €83 to €255/share. I’d love to hear what the analyst forecasting €83 is thinking with regards to his/her model – but suffice to say, I very much disagree with that target.

Since my last article on Rheinmetall, which was close to the beginning of the war, I’ve adjusted my PT’s to reflect the realistic upside that is now there. No, it’s not the straight-line €330/share DCF – that’d be a bit exuberant.

But I’m bumping my conservative PT to €215/share, which I believe reflects a very realistic continued upside for Rheinmetall – close to impressive, double digits for the company. Equity analysts go as high as €230-€250 here, and I don’t really see a problem with those targets, beyond that at those valuations there would be better investments to be made.

Today, at around €190 per share, I consider Rheinmetall a “BUY”.

Thesis

Tempers are heated, and with hot tempers come a hot stock market. Similar to the “nutty” valuations for work-from-home companies we saw during COVID-19, we’re now seeing a massive flow into defense stocks due to geopolitical tensions.

I will be the first one to remind you that much of this premium can be unwound in a relatively short time if things change.

However, I will state to you, dear readers, that we’re seeing a fundamental change in the defense policies of the European Union.

Because of this, which I wrote in my last article, I consider the higher valuations for the companies now justified, and I target an even higher valuation. This paradigm shift makes the company a buy.

I do think that you should still be buying the native though, not the ADR.

Remember, I’m all about:

- Buying undervalued – even if that undervaluation is slight and not mind-numbingly massive – companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

- If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

- If the company doesn’t go into overvaluation but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

- I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

Here are my criteria and how the company fulfills them (bolded).

- This company is overall qualitative.

- This company is fundamentally safe/conservative & well-run.

- This company pays a well-covered dividend.

- This company is currently cheap.

- This company has realistic upside based on earnings growth or multiple expansion/reversion.

[ad_2]

Source link